Advertisement

Fed’s Waller looks for two more 2023 hikes, Bullard steps down; earnings loom – Newsquawk Europe Market Open

- APAC stocks traded mostly higher after the positive lead from Wall St where yields continued to decline post-PPI.

- Fed’s Waller (voter) said the Fed will likely need two more 25bps hikes this year and he favours raising rates at the July FOMC.

- European equity futures are indicative of a slightly lower open with the Euro Stoxx 50 -0.1% after the cash market closed up by 0.7% yesterday.

- DXY remains on a 99 handle, EUR/USD and Cable gain a firmer footing above 1.12 and 1.31 respectively.

- Looking ahead, highlights include US Import & Export Prices, UoM Sentiment (Prelim), Swedish CPI, US Treasury Dealer Meeting Agenda, Earnings from UnitedHealth, JPMorgan, Wells Fargo, BlackRock & Citigroup.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks and bonds ground higher as the cooling inflation momentum followed through to Thursday which was aided by a softer-than-expected PPI release, while the lower jobless claims data did little to derail the momentum with analysts cognizant of the noise around the July 4th holiday.

- SPX +0.85% at 4,510, NDX +1.73% at 15,571, DJIA +0.14% at 34,395, RUT +0.91% at 1,950.

- Click here for a detailed summary.

NOTABLE HEADLINES

- Fed’s Waller (voter) said the Fed will likely need two more 25bps hikes this year and he favours raising rates at the July FOMC, while he is increasingly confident that banking stress won’t derail the economy. Waller added that cooler CPI data is welcome but they need to see if it is sustained, while he doubts core inflation is structurally lower and stated that the September Fed meeting is a live meeting for monetary policy.

- Fed’s Bullard (non-voter) is stepping down effective 14th August 2023, while he has recused himself from his monetary policy role on the FOMC and other related duties and has ceased all public speaking.

APAC TRADE

EQUITIES

- APAC stocks traded mostly higher after the positive lead from Wall St where yields continued to decline as PPI data followed suit to the softer consumer inflation and supported the case for just one more Fed rate hike.

- ASX 200 was firmer with gains in the index led by the tech sector after similar outperformance of US counterparts amid a decline in yields, while the announcement that RBA Deputy Governor Bullock will take over from Governor Lowe in September had little effect on markets and was largely seen as policy continuation.

- Nikkei 225 swung between gains and losses with headwinds from JPY strength and speculation that the BoJ could raise its inflation forecast above the 2% target at its meeting this month, which could pave the way for policy normalisation, while former BoJ Director Hayakawa expects the BoJ to tweak yield curve control at the upcoming meeting by potentially raising the 10yr yield ceiling to 1.0%.

- Hang Seng and Shanghai Comp were positive albeit with gains capped despite the renewed support pledges by the PBoC to keep credit growth appropriate, as well as step up counter-cyclical adjustments and support for key sectors.

- US equity futures lacked firm direction overnight as the focus turns to the US big bank earnings.

- European equity futures are indicative of a slightly lower open with the Euro Stoxx 50 -0.1% after the cash market closed up by 0.7% yesterday.

FX

- DXY remained subdued after slipping to a sub-100 level for the first time since April 2022 as softer PPI data supported the case for just one more rate hike from the Fed, although Fed’s Waller pushed back against this in which he noted the September Fed meeting is a live meeting and that he doubts core inflation is structurally lower now.

- EUR/USD marginally extended on its advances and is on course for its biggest weekly gains in 8 months.

- GBP/USD was uneventful overnight and lingered near the prior day’s best levels after climbing north of 1.3100.

- USD/JPY continued its retreat owing to narrowing yield differentials and amid increasing speculation for potential hawkish forecasts or policy tweaks by the BoJ.

- Antipodeans were kept afloat amid the positive mood but with AUD/USD rangebound and largely unaffected by the announcement of the next RBA Governor, while NZD/USD mildly outperformed despite the holiday in New Zealand.

- PBoC set USD/CNY mid-point at 7.1318 vs exp. 7.1453 (prev. 7.1527)

FIXED INCOME

- 10yr UST futures were contained but held on to the spoils from recent bull-steepening post-inflation metrics.

- Bund futures sat near the prior day’s best levels with prices stuck around the 133.00 level.

- 10yr JGB futures saw early pressure amid the hawkish speculation surrounding this month’s BoJ meeting, but then gradually recovered most of the losses.

COMMODITIES

- Crude futures were quiet and slightly eased back from multi-month highs after rallying yesterday on the back of a weaker dollar, cooler inflation print and reports that Libya’s Sharara oil field is to be halted due to protests.

- Libya’s Sharara oil field (300k bpd) is to be halted due to protests, while production in Libya’s 108 oilfield was also shut down, according to Reuters citing oilfield engineers.

- Qatar set September-loading Al-Shaheen crude term prices at USD 1.68/bbl above Dubai quotes.

- Spot Gold traded sideways despite the continued weakness in the greenback.

- Copper futures plateaued overnight and held on to the recent data-inspired gains.

CRYPTO

- Bitcoin took a breather from yesterday’s gains after crypto assets surged alongside a 96% jump in XRP Token following Ripple Lab’s partial victory against the SEC in which a judge ruled the sale of XRP Tokens on exchanges did not constitute investment contracts.

- Ripple Labs won a case against the SEC whereby a US District Court judge ruled that XRP is not a security in a case brought forth in 2020, according to Cointelegraph.

NOTABLE ASIA-PAC HEADLINES

- PBoC Deputy Governor Liu said China’s overall liquidity is ample and its credit structure improved in H1, while he also noted that financing costs stabilised and dropped in H1. Liu said the PBoC has ample policy tools and will step up counter-cyclical adjustments, as well as improve financial services for tech companies, guide banks to boost lending for tech companies and will increase support for SMEs and the green sector, according to Reuters.

- PBoC official said they will keep credit growth appropriate and step up support for key sectors, while the central bank will deepen interest rate reforms and will guide banks to increase lending to small firms and private firms. Furthermore, the official said there is ample room and various policy tools to cope with challenges, while they will use policy tools such as RRR and MLF, as well as innovate new policy tools if needed, according to Reuters.

- China’s top diplomat Wang Yi said US and China need to take practical actions to bring back ties onto the right track and that the US should adopt a rational and pragmatic attitude and meet China halfway. Wang also said the US must refrain from interfering in China’s internal affairs and stop suppressing China’s economy, trade, and technology, while the US must lift illegal and unreasonable sanctions against China, according to Xinhua.

- India will not impose a countervailing duty on flat rolled steel products from China, according to a Reuters source.

- Australia named Deputy Governor Bullock as the next RBA Governor from September 18th, while Bullock said she is committed to ensuring that the Reserve Bank delivers on its policy and operational objectives.

DATA RECAP

- Singapore GDP QQ (Q2 P) 0.3% vs Exp. 0.3% (Prev. -1.6%)

- Singapore GDP YY (Q2 P) 0.7% vs Exp. 0.6% (Prev. 0.4%)

GEOPOLITICS

- Russian President Putin said new weapons supplies will further escalate the conflict in Ukraine and worsen the situation. It was separately reported that Putin also said he proposed to Wagner fighters at a meeting this month to continue serving in the military, while he added that Russia’s government and parliament must discuss the legal framework for private armies and said without a legal framework, ‘Wagner does not exist’, according to Kommersant.

- Kremlin spokesman said there is no final decision yet on withdrawing from the Black Sea grain deal.

Did Costco Hit Bud Light With “Death Star”?

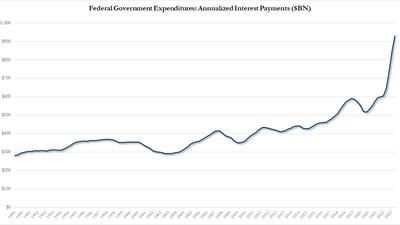

Did Costco Hit Bud Light With “Death Star”?  Endgame: US Federal Debt Interest Payments About To Hit $1 Trillion

Endgame: US Federal Debt Interest Payments About To Hit $1 Trillion