Advertisement

Equities lower, AUD lags post-RBA; US ISM, JOLTs data & earnings due – Newsquawk US Market Open

- European bourses are in the red with initial catalysts light but sentiment deteriorating further alongside Final PMIs

- Stateside, futures also pressured but magnitudes are more contained ahead of manufacturing data

- DXY continues to climb to the detriment of G10 peers, AUD lags post-RBA maintained its Cash Rate

- EGBs slip despite deteriorating risk and welcome EZ PMI commentary re. inflation; USTs mixed

- Crude slumps as sentiment slips and the USD remains bid with metals also dented

- Looking ahead, highlights include US ISM, JOLTS, New Zealand Labour Data, Speech from Fed’s Goolsbee. Earnings from American International Group Inc, Advanced Micro Devices Inc, Electronic Arts Inc, Merck & Co Inc.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are in the red, Euro Stoxx 50 -1.0%; as sentiment has deteriorated gradually since the European cash open and was impacted further by the morning’s Final PMIs.

- Sectors are similarly negative, with Autos lagging amid marked losses in BMW despite a guidance update as associated H2 commentary flagged headwinds. Basic Resource names are similarly dented post-Fresnillo.

- To the upside, Energy is the only sector in the green bolstered by Q2 earnings from BP who announced a buyback and increased their dividend while Banks derive support from HSBC.

- Stateside, futures are modestly softer and have been drifting in-line with European peers throughout the morning but with magnitudes more contained ahead of key data points; ES -0.3%.

- Click here for more detail.

- Click here and here for a recap of the main European equity updates.

FX

- A session of firm gains thus far for the Dollar amid the broader risk aversion across the market coupled with continued weakness in the JPY against major peers.

- Antipodeans remain the marked laggards amid a combination of subdued risk and RBA opting to pause.

- Traditional havens are also on the back foot against the Dollar but to a lesser extent vs the non-US dollar counterparts. JPY continues to feel headwinds following the BoJ policy decision and subsequent off-schedule bond purchases conducted yesterday.

- EUR and GBP are subdued against the Dollar with little initial reaction seen to the final release of the S&P Manufacturing PMIs, which underscored increasing risks of recession, although prices have been moving favourably amid sharply deteriorating demand.

- PBoC set USD/CNY mid-point at 7.1283 vs exp. 7.1495 (prev. 7.1305)

- Click here for more detail.

- Click here for the Option Expires for the NY Cut.

FIXED INCOME

- EGBs slip while USTs are mixed/tentative with drivers limited overall ahead of a busy PM agenda; EGBs are under bearish pressure despite deteriorating risk sentiment and welcome EZ PMI commentary re. inflation.

- Bunds at the lower-end of 132.64-133.06 parameters with attention still on Friday’s 131.81 low, specific catalysts remain light aside from the referenced PMI commentary.

- USTs are more mixed with the short-end bid and the long-end soft though magnitudes are relatively minimal and from a yield perspective it is only resulting in very modest curve flattening

- Click here for more detail.

COMMODITIES

- WTI and Brent front-month futures are modestly softer intraday as the Dollar remains firm and risk sentiment tilts lower.

- Spot gold is pressured by the firmer Dollar awaiting the US ISM and JOLTS data, with the yellow metal sandwiched between its 100 and 21 DMAs at USD 1,968.25/oz and USD 1,950.60/oz respectively.

- Base metals are on the back foot amid the broader risk aversion, stronger Greenback, and the surprise contraction in the Caixin Manufacturing PMI.

- Click here for more detail.

NOTABLE US HEADLINES

- Blackrock (BLK) and MSCI (MSCI) face congressional probes for facilitating China investments, according to WSJ.

- Amazon (AMZN) is planning to invest some USD 7.2bln in Israel through 2037, according to local press.

- Tesla (TSLA) is reportedly seeking almost USD 100mln from the US to build a semi-truck charging route from Texas to California, according to Bloomberg citing emails.

- Click here for the US Early Morning note.

NOTABLE EUROPEAN HEADLINES

- Germany’s VDMA says German engineering orders in June -15% Y/Y (domestic -18%; Foreign -14%).

- German Economy Ministry says the European Commission has made important progress on subsidies for hydrogen power plant talks, but no approval yet.

DATA RECAP

- EU HCOB Manufacturing Final PMI (Jul) 42.7 vs. Exp. 42.7 (Prev. 42.7); ECB “will be pleased to see that deflation of output prices has picked up speed again, falling at the most rapid pace in almost 14 years.

- EU Unemployment Rate (Jun 2023) 6.4% vs. Exp. 6.5% (Prev. 6.5%).

- German Unemployment Change SA (Jul 2023) -4.0k vs. Exp. 20.0k (Prev. 28.0k); Unemployment Rate SA (Jul 2023) 5.6% vs. Exp. 5.7% (Prev. 5.7%)

- UK S&P Global/CIPS Manufacturing PMI Final (Jul) 45.3 vs. Exp. 45.0 (Prev. 45.0); July saw little movement in selling prices.

- UK BRC Retail Shop Price Index YY (Jul) 7.6% (Prev. 8.4%)

- UK food price inflation has slowed to its lowest level this year in July, at 13.4% (vs 14.6% in June), according to BRC and NielsenIQ retail analysts.

- UK Lloyds Business Barometer (Jul) 31 (Prev. 37)

GEOPOLITICS

- White House’s Kirby said the US is not encouraging attacks inside Russia and that the decision is for Ukraine to make, according to a CNN interview.

- A drone hit a high-rise building in Moscow and a second drone was downed in Moscow’s suburbs, according to agencies quoting emergency services.

- China’s Defence Ministry said it lodged solemn representations to the US side regarding US military arms sales to Taiwan and urges the US to stop all forms of military collusion with Taiwan, according to Reuters.

CRYPTO

- The ‘Ripple ruling’ on crypto was rejected by a federal judge in the Terra case whereby the judge ruled that there is no distinction between public and institutional sales, according to Bloomberg.

APAC TRADE

- APAC stocks were mostly higher following the positive lead from Wall St where the S&P 500 notched its 5th consecutive monthly gain, while participants also digested disappointing Chinese Caixin Manufacturing PMI data and the RBA rate decision.

- ASX 200 traded positive amid strength in tech and the commodity-related sectors with further upside after the RBA kept rates unchanged.

- Nikkei 225 was underpinned by a weaker currency and with headlines in Japan dominated by earnings releases, while a recent poll by Bloomberg also showed that BoJ watchers don’t expect a further policy shift from the central bank this year with April 2024 now seen as the likely timing for a policy change

- Hang Seng and Shanghai Comp managed to shrug off the disappointing Chinese Caixin Manufacturing PMI data which slipped into contraction territory for the first time in 3 months with Hong Kong boosted by tech strength and the mainland kept afloat by further support efforts from China.

NOTABLE ASIA-PAC HEADLINES

- China’s NDRC issued a notice to promote private economy development in China and said it will extend loan support tools for small and micro firms until the end of 2024.

- RBA maintained its Cash Rate Target unchanged at 4.10% (vs split views between 25bps hike and unchanged) and noted that some further tightening of monetary policy may be required. RBA reiterated that the Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that, while it also reaffirmed a priority to return inflation to target within a reasonable timeframe and expects inflation will be back at 2-3% target range in late 2025.

DATA RECAP

Advertisement

- Chinese Caixin Manufacturing PMI Final (Jul) 49.2 vs. Exp. 50.3 (Prev. 50.5)

- Australian Building Approvals (Jun) -7.7% vs. Exp. -7.0% (Prev. 20.6%)

Exxon About To Become ‘Lithium Kingpin’? Talks Begin With Tesla, Ford, Volkswagen, Reports Say

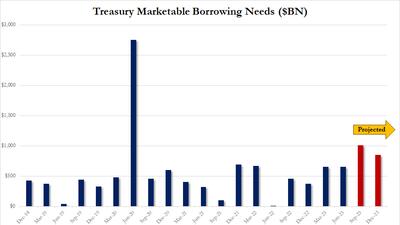

Exxon About To Become ‘Lithium Kingpin’? Talks Begin With Tesla, Ford, Volkswagen, Reports Say  Debt Tsunami Begins: US To Sell $1 Trillion In Debt This Quarter, 2nd Highest In History, As Budget Deficit Explodes

Debt Tsunami Begins: US To Sell $1 Trillion In Debt This Quarter, 2nd Highest In History, As Budget Deficit Explodes