Advertisement

Binance has quietly laid off 1,000 or more employees in recent weeks; may slash workforce by up to 30%: WSJ

Binance has sacked more than 1,000 people in recent weeks as it contends with regulatory and legal hurdles in the U.S. and other jurisdictions, the Wall Street Journal reported July 14, citing a person familiar with the matter.

The exchange had roughly 8,000 employees around the globe before the layoffs began a few weeks ago. Sources told the newspaper that the firing could continue until the exchange’s global workforce is reduced by a third.

According to the report, the exchange has cut people across the board throughout its various global operations, but customer service roles were affected the most.

Binance confirmed the layoff but did not specify how many roles were cut. A spokesperson for the exchange told WSJ:

“As we prepare for the next major bull cycle, it has become clear that we need to focus on talent density across the organization to ensure we remain nimble and dynamic. This is not a case of rightsizing, but rather, re-evaluating whether we have the right talent and expertise in critical roles.”

The cuts have been happening at the same time as multiple executives stepping down from their roles at the exchange. It is unclear whether the high-profile departures were part of the overall layoffs.

WSJ reported at the time that their departures were motivated by worries over the U.S. Department of Justice levying criminal charges against Binance and its founder Changpeng ‘CZ’ Zhao.

CZ and one of the executives said the claims were unfounded and labeled them fear-mongering by the media.

European operations slowing

Binance has had to pull out of multiple jurisdictions — primarily in Europe — in recent weeks after failing to secure licenses and approvals for its operations. It is also contending with regulatory and legal pressure in the U.S.

The exchange had bustling and massive operations across the globe until recently, and the run-in with regulators could be part of the reason behind reevaluating its workforce.

Advertisement

Binance has so far pulled out of the Netherlands, Germany, Cyprus, Austria, and Belgium due in recent weeks due to various reasons.

The exchange said it is shifting its focus to ensuring its ready for the upcoming Markets in Crypto Assets (MiCA) rules, which come into force in 2024 and will establish a framework of regulation and licensing for the industry.

Firms that meet the MiCA requirements will be able to operate across all EU nations via one license, and many, including Binance, are already prepping for the upcoming rules.

Binance saw nearly $2 billion in inflows in the last 24 hours, according to DeFillama data, despite the alleged FUD surrounding the exit of its key executives.

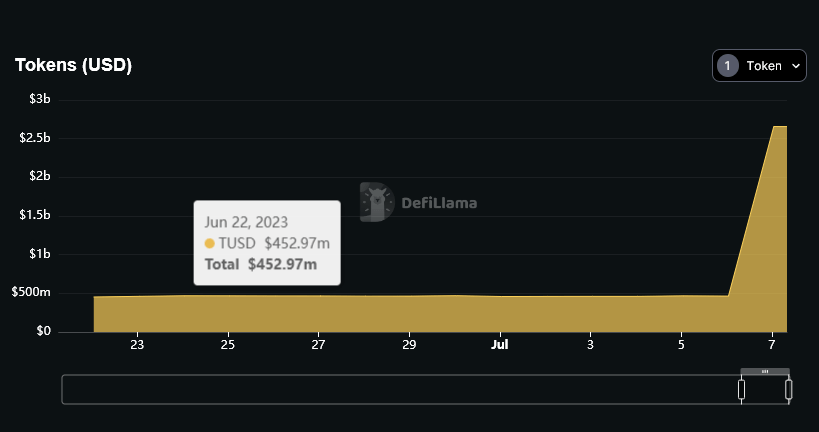

Binance TUSD’s balance skyrockets.

The inflow can be attributed to the massive spike in the exchange’s TrueUSD (TUSD) balance during the last 24 hours.

TUSD’s balance on Binance jumped to $2.65 billion from less than $500 million recorded on June 6, according to DeFillama data.

Source: DeFillama

Source: DeFillama

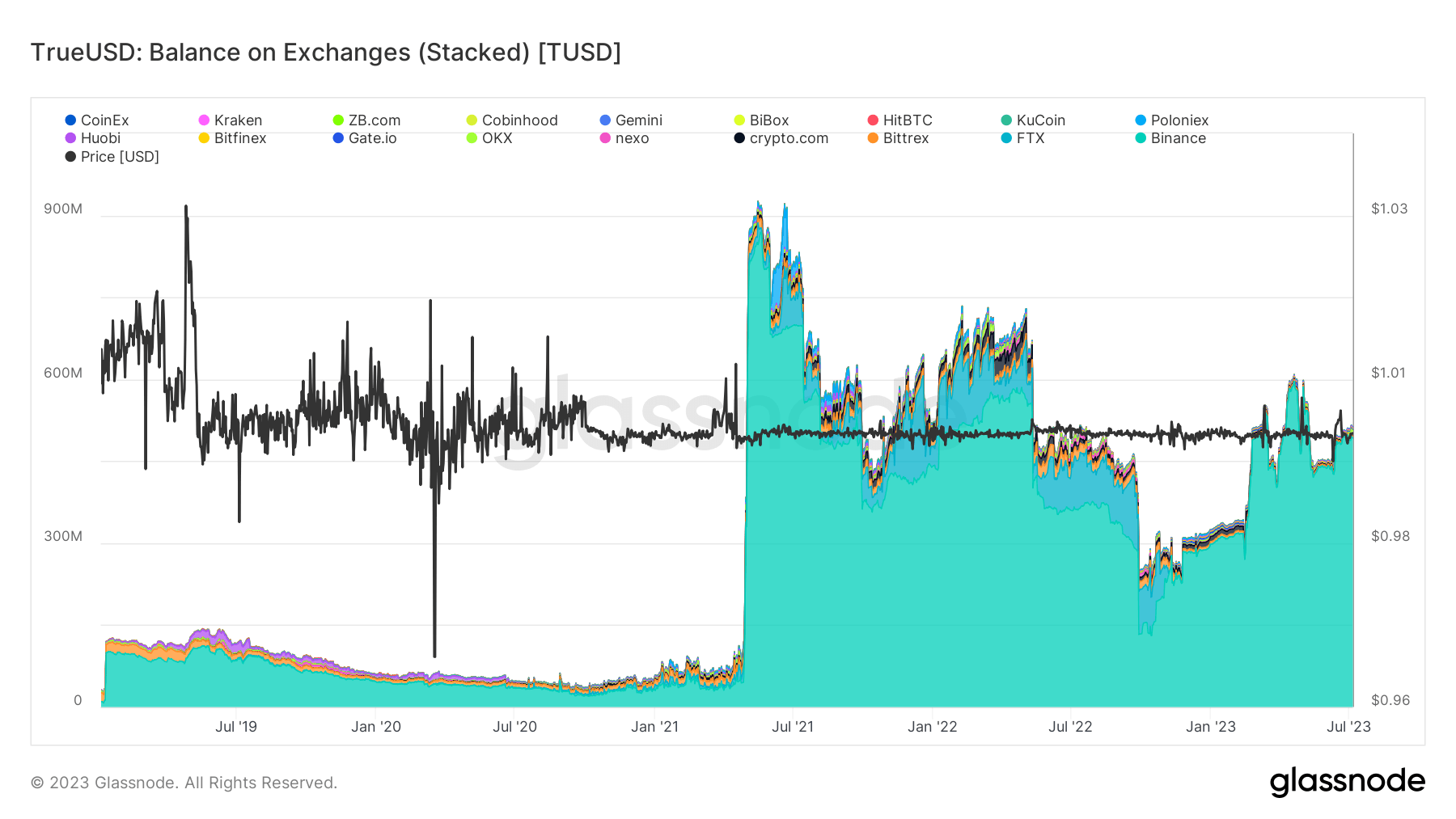

Meanwhile, data from Glassnode shows that TUSD’s total balance across all exchanges is $512.92 million as of July 6. However, $498.58 million, representing 96% of the $512.92 million balance, is on Binance.

Source: Glassnode

Source: Glassnode

Other exchanges like OKX, Bitfinex, Gate.io, Huobi, and others hold less than $20 million of the stablecoin.

Since Binance USD’s (BUSD) struggles began with regulators, Binance mainly promoted TUSD as its successor for the embattled stablecoin. The exchange has minted more of the TUSD stablecoin and added new trading pairs for the asset.

TUSD has faced increased scrutiny over its alleged ties to Justin Sun and its exposure to the insolvent crypto custodian, Prime Trust.

Binance was yet to respond to CryptoSlate’s request for comment at the time of writing.

CZ addresses key executives leaving.

Meanwhile, Binance CEO Changpeng ‘CZ’ Zhao said the reasons attached to the company’s key executives’ exits were “completely wrong.”

On July 6, Binance chief strategy officer Patrick Hillmann and the exchange’s senior vice president for compliance Steven Christie confirmed they were leaving the platform.

While some crypto community members quickly linked their exits to the exchange’s recent regulatory challenges, the executives stated they left the firm on good terms.

In his July 7 statement, CZ described the outcry surrounding these exits as another FUD, adding that every company experiences turnover. CZ thanked the exiting executives for their services and assured users that the platform can ” protect our users at all times.”

“As markets and the global environment for crypto changes, as our organization evolves, and as personal situations change, there is turnover at every company.”