Advertisement

The Great Forecast Fiasco: What Went Wrong with Bitcoin Price Forecasts in 2025?

Under the friendliest crypto administration yet, the Bitcoin price is heading for a negative returns closure this year, presently at -7.6% and trading at ~$88k. This is in stark contrast to solid yearly gains in 2023 and 2024, at +146.8% and +135% respectively.

During the crypto bankruptcy cascade throughout 2022, starting with Terra (LUNA) and finishing with the FTX exchange fiasco, Bitcoin had one of its worst years, ending at -62%. Only 2018 was worse (the worst ever) at -72.1%.

In this context, a single-digit dip into the negative zone doesn’t look bad. However, it is still at severe odds with Bitcoin price predictions made throughout 2025. More tellingly, this happened in the absence of any FTX-like events.

Rather than chasing the next forecast, the more revealing exercise is to examine why previous price predictions failed so comprehensively. First, let’s revisit Bitcoin price predictions from notable institutions.

Bitcoin Price Predictions in 2025: Why Institutional Forecasts Matter

While Bitcoin price predictions should always be treated with a grain of salt, those originating from established financial institutions remain more worthy of scrutiny. After all, having reputational constraints, formal research standards and regulatory oversight imposes some degree of discipline compared to random blogs and YouTubers.

With that in mind, here is how big players reasoned Bitcoin priced by the end of 2025:

- Standard Chartered: $200,000 based on corporate treasury demand, crypto-friendly Trump administration and ETF flows. Only in December did the bank cut this forecast by half to $100,000. By the end of 2026, the new target is now $150,000.

- VanEck: $180,000 based on strong institutional inflows and Bitcoin mining resilience despite mining difficulty hitting new highs.

- JPMorgan: $165,000 based on Bitcoin’s risk profile being similar to gold. Interestingly, the bank forecasted Bitcoin to outperform gold in H2, while the opposite transpired. JPMorgan’s long-term BTC price target is $240,000.

- Bernstein: $200,000 based on strong institutional demand and Bitcoin’s role as an inflation hedge. The bank now forecasts $150,000 by the end of 2026, which is cut in half from the previous $300,000 level.

- Fundstrat: $250,000 based on post-halving supply shocks and the U.S. Bitcoin Reserve narrative, alongside rising institutional inflows via ETFs.

- Ark Invest: $1.5 million by 2030 for the bull case, which would imply a target of ~$124,000 by the end of 2025. For the bear case of $300,000 by 2030, the implied target would be ~$91.5k by the end of 2025, making this one of the most accurate forecasts (for the bear case). Cathie Wood’s signed reasoning is similar to others – corporate treasuries, institutional inflows, digital gold and emerging market safe haven.

Between the six financial institutions, the average Bitcoin price forecast by the end of 2025 was $181k, if we include Ark Invest’s bare case as the most accurate outlier. This means that institutions wrongly predicted Bitcoin’s price move by the end of 2025 by 80%, if we assume the Bitcoin price will hold by the year’s end at around $88k.

Why the Institutional Consensus Failed

As is clear from the institution’s shared reasoning on Bitcoin’s price appreciation, they put much weight on institutional inflows. This formed a homogenized forecasting logic. However, these expectations were largely priced in even before 2025.

In other words, once the ETFs launched, the market required an “exceeding expectations” narrative instead of just “meeting expectations” for the parabolic rise to continue. It is exceedingly difficult to say that Bitcoin ETF flows either mirror BTC price or cause it.

Rather, it is more accurate to say that the relationship between Bitcoin ETF inflows/outflows and BTC price is a reflexive feedback loop – both causing and mirroring each other.

Advertisement

Specifically, when the Bitcoin price starts to rise, due to news, macroeconomic narrative, or technical momentum, the positive media coverage tends to kick in, inciting more investors to dip in. Other way around, when the Bitcoin price starts to plummet, panic-selling tends to kick in for both retail and institutional investors.

Another way to describe this dynamic is the interplay between supply shock and demand exhaustion.

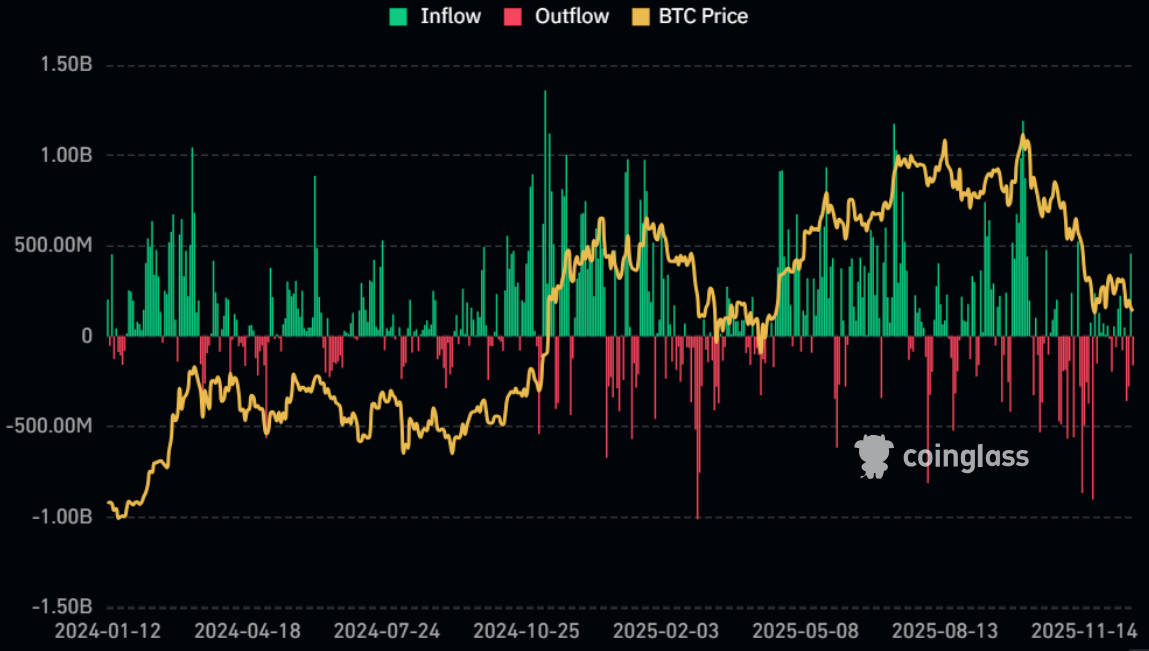

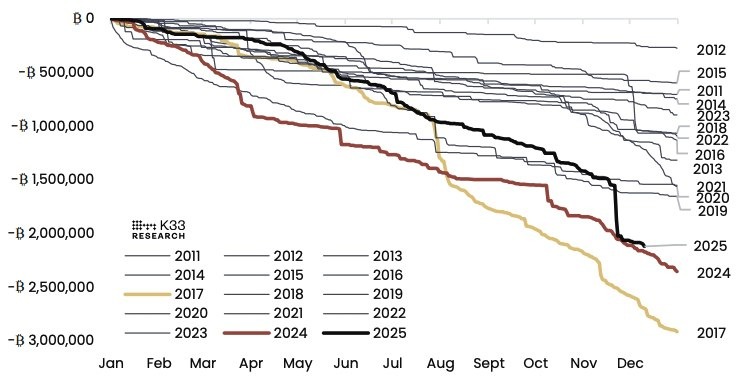

However, this dynamic is nothing new as, historically, long-term holders (LTH) buy up the panic-selling of short-term holders (STH). Yet, since the October price crash, LTH (holding over 155 days) has been exerting a sustained selling pressure as K33 Research recently noted.

In particular, K33 researcher Vetle Lunde noted that 1.6 million BTC from LTH returned into circulation in 2024. As shown on the chart above, this is the largest LTH reallocation since 2017. This amount of Bitcoin is roughly $130 billion, representing a significant percentage of the liquid supply and Bitcoin’s $1.76 trillion market cap.

There are two likely triggers for this dynamic that ended up leveling down Bitcoin price post-October:

- Profit-taking from the crossed psychological milestone above $100,000.

- President Trump’s abrupt Truth Social threat to increase tariffs on Chinese imports by extra 100% – constituting a major geopolitical risk shock.

Although, by the end of October, President Trump and Chinese President Xi Jinping came to an agreement, the damage was already done as evidenced by the liquidation spree of nearly $20 billion worth of options.

It should also be noted that Trump’s second term has been one of the most openly transactional presidencies on record. After all, he amassed significant wealth since the launch of his TRUMP token through World Liberty Financial, NFTs and related deals after his reelection.

This is on top of Trump’s repeated open admissions to receiving millions from Miriam Adelson:

“Miriam and Sheldon would come into the office. They’d call me. They’d call me. I think they had more trips to the White House than anybody. Look at her sitting there so innocently. She’s got sixty billion in the bank. Sixty billion.”

President Trump speaking at Knesset in October 2025

Given the nature of President Trump’s presidency, and his revealed character from the days of World Wrestling Entertainment (WWE), it is very likely he would say things that would trigger financial events, which would then benefit his inner circle – be they related to stocks or Bitcoin.

Of course, it is exceedingly difficult to predict such moves by any forecaster as they technically constitute black swans.

The Bottom Line

The average $181k Bitcoin forecast failure is a trifecta of factors that overwhelmed simplistic “ETF demand” narrative, alongside the “Bitcoin treasuries” narrative. First, the initial ETF hype was already priced in. Second, a historic scale of sustained profit-taking by LTH. Third, fumbled by politically generated, un-forecastable black swan events.

This trifecta continues to exert mass de-leveraging and options liquidation. On the upside, K33 Research also points that profit-taking from early holders is largely over. If true, this marks an exhaustion point.

But more importantly, deep institutional liquidity that allowed this process in the first place demonstrates that Bitcoin greatly matured. That maturity, however, also sharpens the contrast between speculative assets and long-term strategies such as dividend investing, where returns are less dependent on forecasting precise price targets.

The lesson for 2026 forecasting is clear: future price predictions must move beyond linear demand models and account for the reflexive nature of ETF flows and the LTH exhaustion dynamic when new price thresholds are reached.

At the end of the line, all revised forecasts are still bullish from the present price point. This should surprise no one as it is impossible for any government, within the mass democracy framework, to become fiscally responsible. This means that people will continue to seek safe haven outside of fiat currencies.

Author

Shane Neagle

Shane Neagle is the Editor in Chief of The Tokenist, a digital publication focused on the evolving intersection of finance and technology. Originally from Maine, Shane’s career began in the U.S. Army, where he served as an intelligence analyst before transitioning to work with various Department of Defense contracting companies. His experiences analyzing complex information in high-stakes environments laid the foundation for his deep interest in global systems and economic dynamics. Shane holds a bachelor’s degree in philosophy from KU Leuven. He is particularly fascinated by the rapid pace of technological advancement and its ability to redefine long-standing paradigms in finance and macroeconomics. At The Tokenist, he leads editorial strategy with a commitment to clarity, depth, and forward-thinking insights at the intersection of digital assets, markets, and innovation.